Navigating the healthcare system in the United States often feels like learning a completely new language. Between premiums, deductibles, and co-pays, the financial side of healthcare requires careful attention. When you need hospital treatment, another critical term enters the vocabulary: pre-authorization.

Pre-authorization is an approval process required by your health insurance company before you receive specific medical services, treatments, or medications. It acts as a gateway, ensuring the proposed hospital treatment is medically necessary and covered under your specific health plan.

Healthcare costs in the United States are exceptionally high. Insurance companies use pre-authorization as a cost-control measure to prevent unnecessary procedures and to ensure that cheaper, equally effective alternatives are considered first. While it can seem like a frustrating hurdle, understanding the process can save you a tremendous amount of stress.

Failing to secure this approval can have severe financial consequences. If you proceed with a hospital treatment without the required pre-authorization, your insurance company can legally refuse to pay the bill. This leaves you completely responsible for the out-of-pocket costs, which can easily reach tens or hundreds of thousands of dollars for hospital stays.

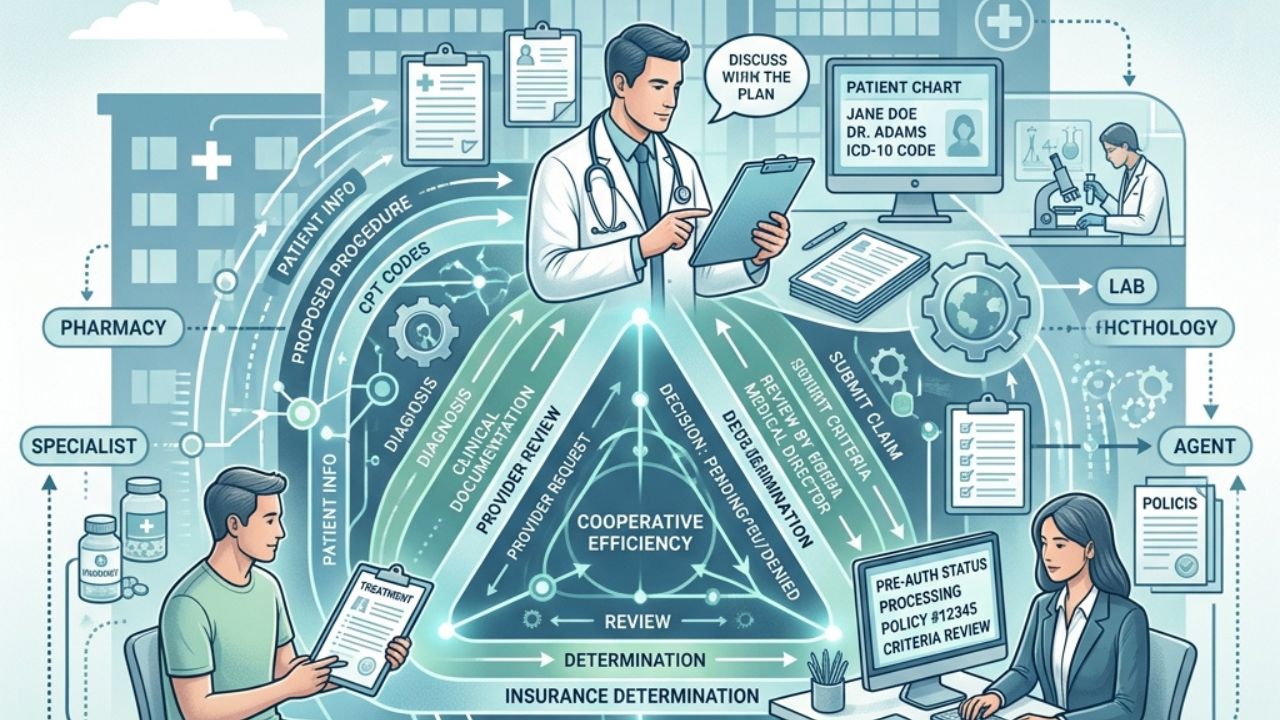

Key Players in the Pre-Authorization Process

Securing approval is a team effort. Understanding who does what will help you monitor the process and step in if delays occur.

The Patient’s Role

As the patient, you are your own best advocate. While you rarely submit the paperwork yourself, you hold the ultimate responsibility for ensuring the approval is in place before your treatment begins. You must understand your insurance policy, ask your doctor the right questions, and follow up relentlessly.

The Provider’s (Doctor/Hospital) Role

Your healthcare provider handles the heavy lifting of the pre-authorization request. The doctor or hospital staff gathers your medical records, test results, and clinical notes to prove that the treatment is medically necessary. They submit this clinical evidence directly to your insurance company.

The Insurance Company’s Role

The health insurance company acts as the reviewer. Their medical directors and claims adjusters evaluate the clinical information submitted by your doctor. They compare this data against their own medical policies and your specific coverage benefits to determine if the treatment will be approved or denied.

Step-by-Step Guide to Getting Pre-Authorization

Taking a systematic approach ensures you do not miss critical details. Follow these steps to navigate the approval process successfully.

Step 1: Verify Your Insurance Policy

The very first thing you need to do is understand the rules of your specific health plan.

Understanding your benefits and coverage

Call the member services number on the back of your insurance card. Ask for a detailed explanation of your hospital benefits. You need to know your deductible status, your coinsurance percentage, and your out-of-pocket maximum.

Identifying services requiring pre-authorization

While on the phone with your insurer, ask exactly which services require prior approval. Routine check-ups rarely need it, but scheduled surgeries, advanced imaging (like MRIs or CT scans), and inpatient hospital stays almost always do. Request a written copy of these requirements for your records.

In-network vs. Out-of-network providers

Confirm that your hospital and your primary surgeon are in-network. Insurance companies have strict rules regarding out-of-network care. Even if an out-of-network treatment is pre-authorized, your financial burden will be significantly higher.

Step 2: Consult with Your Healthcare Provider

Once you understand your insurance requirements, discuss them with your doctor. Inform them that your plan requires pre-authorization for the proposed treatment. Ask them about their office’s timeline for submitting the paperwork. Establish a clear line of communication with the specific staff member responsible for handling billing and approvals.

Step 3: Monitor the Submission and Review

Do not simply assume the paperwork was sent. Call your provider’s office a few days after your appointment to confirm the pre-authorization request was submitted. Then, call your insurance company to confirm they received it. Ask the insurer for an estimated timeline for their decision. Standard reviews can take up to 14 days, though urgent requests can be expedited.

Step 4: Obtain the Authorization Number

When the insurance company approves the treatment, they issue a specific authorization number. You must get this number and keep it safe. Bring it with you to the hospital on the day of your treatment. This number is your proof that the insurance company agreed to cover the procedure.

Frequently Asked Questions

What happens if my pre-authorization is denied?

If your request is denied, you have the right to appeal the decision. The insurance company must provide a specific reason for the denial. Often, denials occur simply because the doctor’s office failed to send enough medical documentation. You and your doctor can gather more evidence and submit a formal appeal.

Does pre-authorization guarantee full payment?

No. Pre-authorization only guarantees that the service is covered under your plan. You are still responsible for your standard deductibles, co-pays, and coinsurance amounts as dictated by your policy.

Can pre-authorization be done retroactively?

In cases of a true medical emergency, insurance companies usually waive the immediate pre-authorization requirement. However, you or a family member must notify the insurance company within a specific window (usually 24 to 48 hours) after admission. For non-emergencies, retroactive authorization is extremely rare and usually results in denied claims.

Taking Control of Your Medical Care

The pre-authorization process demands patience and vigilance. By actively participating in the steps, communicating clearly with your doctor, and holding your insurance company accountable, you can protect yourself from unexpected medical debt. Always document your phone calls, keep records of who you spoke with, and never hesitate to ask questions until you fully understand your coverage.